The HELOC Journey with SFCU, Made Easy!

March 9, 2026

What Is a HELOC?

A Home Equity Line of Credit (HELOC) gives you access to a revolving line of credit that you can draw from as needed. It works a bit like a credit card but typically offers a lower rate because it’s secured by your home’s equity. You can borrow as much or as little as you need up to your approved limit, and you only pay interest on the amount you use. This post is for education only and is designed to help you understand what a HELOC is and what the general journey looks like when you explore one.

HELOCs are often used for:

- Home Improvements

- Education Expenses

- Weddings

- Family Vacations

- and more!

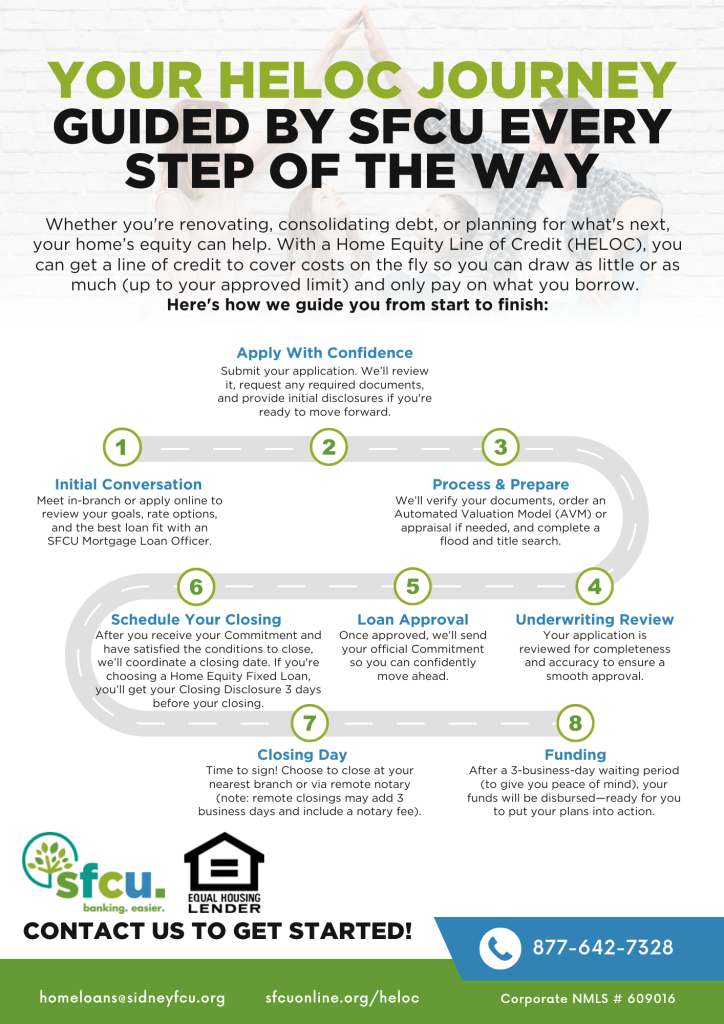

Your HELOC Journey

Below is an educational walkthrough of the typical steps involved in opening a HELOC. These steps reflect the experience shared by SFCU mortgage representatives and your provided process information.

1. Start the Conversation

Your journey begins with a conversation about your goals. During this step, you meet with a mortgage loan representative who explains rate options, timelines, and whether a HELOC could fit your needs.

2. Submit Your Application

Next, you complete your application. SFCU mortgage representatives guide you through the process and help ensure everything is submitted correctly.

3. Property Valuation & Documentation

After you apply, the lender reviews your documents. They may also order an Automated Valuation Model (AVM) or a full appraisal. Additionally, a title search and flood certification are typically completed during this stage.

4. Underwriting Review

Then, underwriting reviews your file for accuracy and completeness. This step helps ensure your application is ready for approval without delays.

5. Approval & Commitment

Once your HELOC is approved, you receive an official Commitment that explains your terms.

6. Schedule Your Closing

After approval, you schedule your closing. You can choose an in‑branch appointment or a remote notary option, though remote closings may require extra time and include a notary fee.

7. Closing Day

On closing day, you sign the final documents, and your HELOC becomes officially established.

8. Funding (After a Waiting Period)

Finally, after a required three‑business‑day waiting period, your HELOC becomes active. At that point, you can draw funds as needed for eligible expenses such as home improvements, medical costs, vacations, education, and more.

Take the First Step

If you’re ready to continue your HELOC journey, taking the first step is simple. You can reach out to an SFCU mortgage representative for guidance, or apply online anytime to start exploring your options. SFCU’s team is known for helping members through the application process, which makes getting started easier than you might expect.

Start Your Journey: Apply Here!

Test Modal

Modal Content

Ea rerum vel molestiae omnis molestias. Et ut officiis aliquam earum et cum deleniti. Rerum temporibus ex cumque doloribus voluptatem alias.

Let's Get Started!

Not a Member?

We’d love to welcome you to the SFCU family! Getting started is easy – just click the link below to begin opening your account.

Already a Member?

Head over to online or mobile to add a new product. See ‘xPress Accounts’ under ‘Account Services’ Menu. Or select ‘Add a Product’ to get started now.

Leaving Our Website

You are leaving our website and linking to an alternative website not operated by us. We do not endorse or guarantee the products, information, or recommendations provided by third-party vendors or third-party linked sites.